9 Fees You Should Never Pay Your Merchant Services Provider

Deciding which payment methods to accept for your business? It can be a tough choice.

Operating a cash-only business is basically a death knell. Sure, you bypass credit card processing set up, fees and middlemen, but Americans are using cash less often, according to Gallup, and mobile payments are on the rise.

That said, there are a number of landmines to navigate when it comes to credit card processing, like picking the right provider and rate plan for your business. Making the wrong choice could lead to numerous headaches in the form of painful terminal leases, unfair contract terms, dishonest billing practices and lost profit.

Merchant billing statements are incredibly confusing, which makes it all too easy for your provider (whether it’s a Merchant Account Provider or Payment Facilitator) to take advantage of you. Some fees are legitimate pass-through fees, whereas others simply boost your provider’s bottom line.

The following fees are blatant examples of unethical billing practices (read more about each fee here). If you spot any of these fees on your merchant statements, you’re not working with an honest provider.

- PCI Compliance Fee

If your business is categorized as non-compliant with the Payment Card Industry Data Security Standards, a yearly or monthly fee can be added to your merchant statements. This fee simply penalizes you for not verifying your compliance. The card brands (Visa, MasterCard, Discover and AmEx) are not charging your provider this fee.

Fair providers work with their customers to help them achieve compliance.

- Self-Assessment Questionnaire (SAQ) Fee

This fee is imposed on businesses that don’t complete an SAQ to verify their PCI compliance. It essentially dings businesses twice for the same issue and can be charged quarterly or monthly until an SAQ is submitted.

The SAQ is a self-assessment, so there’s no valid reason for your provider to bill you.

- Next-Day Funding Fee

It doesn’t cost your provider anything to offer your business next-day funding. However, unethical providers get away with this fee by making it seem like a premium service. You should never be charged to simply access your money when it’s available.

- Address Verification System (AVS) Fee

A fraud-prevention measure, AVS ensures that the billing address provided by a customer matches the address associated with the card used for the purchase. It’s a best practice for card-not-present transactions and costs just $0.01 to implement.

Some providers assume their customers don’t know the true cost of this service and inflate this fee.

- Padded Dues and Assessments

The card brands charge dues and assessments to providers to cover marketing expenses, price and rule setting, network operations and fraud-prevention research. This fee is standardized for all providers and is published on each card brand’s Interchange guide.

Visa, MasterCard and Discover charge between 0.11% and 0.13% for dues and assessments. AmEx charges 0.15%. Unethical providers assume business owners don’t know these rates offhand, and inflate this pass-through fee to make an extra buck.

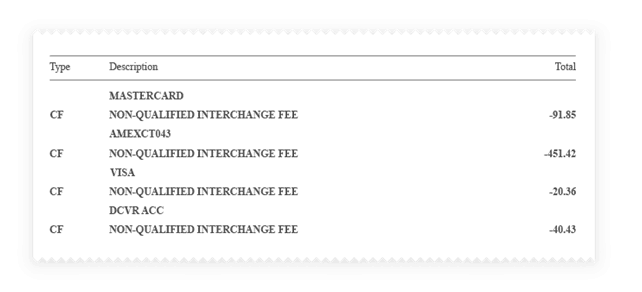

- Non-Qualified Interchange Fee

This fee is tricky. It borrows terminology from one rate plan and applies it to another. On Tiered rate plans, transactions are bundled into Non-Qualified, Mid-Qualified and Qualified transactions based on risk and reward. On Interchange-plus pricing, there’s no such thing as a Non-Qualified transaction, much less a fee.

Some providers charge this for each of the major card brands, costing business owners hundreds.

- EMV Compliance Fee

Many businesses have EMV-ready terminals but still can’t accept EMV cards. This is largely due to backed up certification queues. It’s the provider’s responsibility to get certified, but some penalize their customers with a fee.

- Inactivity Fee

Different from a minimum-processing fee that covers the cost to keep the merchant account open, an inactivity fee is charged by some providers when their customers don’t take any credit or debit card transactions within a given period of time.

There is no cost to offset, so your provider should never charge you this fee.

- Tax Reporting Fee

All providers are legally required to report your revenue to the IRS; however, some see this as an opportunity to hit you with a fee under the guise that this is a service for which you need to pay.

Look at your merchant statements with a critical eye and question each fee listed. If you spot any of the fees detailed above, it’s worth switching to a provider that believes in ethical and transparent billing.

ABOUT THE AUTHOR

Christina Lavingia is the marketing manager at PayJunction. With a background in personal finance, her commentary and articles have been published on Forbes, U.S. News, AOL Finance, CBS News, The Huffington Post and more.