Whether you’re employed by a company or you’re employing yourself, retirement is something you must plan for. Forbes takes a look at three retirement plans that can be used to help you set up a fund for yourself or your employees.

The 401(k)

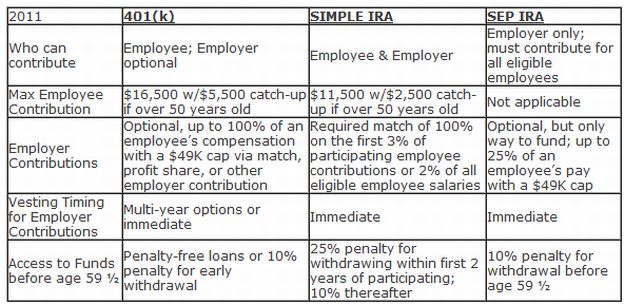

401(k)s not only offer higher contribution limits than most other plan options, but also offer more choices in design to manage business costs and program saving goals. You can choose to match or not, provide a vesting schedule, or enable penalty-free access to funds via a loan if an emergency arises. 401(k) plans also allow for “catch-up†contributions after reaching the age of 50. In 2011, employees can contribute up to $16,500 if under 50 years of age, $22,000 if over.

For small businesses and employees that may fear higher tax rates down the road, the Roth 401(k) enables participants to have their contributions taxed up-front, but withdrawals in retirement are tax-free, earnings and all. This can be a big help in managing your tax situation and money over time.

SEP IRAs

It doesn’t have all the bells and whistles of a 401(k) plan, but it’s got a good engine under the hood. One of the most important things to understand about SEPs is that 100 percent of the contributions made are by the employer (no employee contributions allowed) and these dollars are immediately vested for the employee.

The SIMPLE IRA

The SIMPLE IRA’s name … stands for Savings Incentive Match Plan for Employees. While both employer and employee can contribute to the plan, the employer must match and matching is vested immediately. Also, the employee contribution limit is set at $11,500 for 2011, a full $5,000 less than a 401(k).

Photo by Pug50